London’s March Auctions Show Blue-Chip Art Operating as Financial Infrastructure

Strong March evening sale results in London point to a market that is less speculative and more aligned with wealth preservation, collateral strategy, and estate planning.

London’s March modern and contemporary evening sales delivered a result that looked contradictory on the surface and coherent underneath. Even as geopolitical stress intensified, the high end of the market absorbed major consignments with discipline. According to reported figures, Sotheby’s and Christie’s posted sharp year-on-year gains for equivalent spring sales, while sell-through stayed high in sessions supported by guarantees and curated lot management.

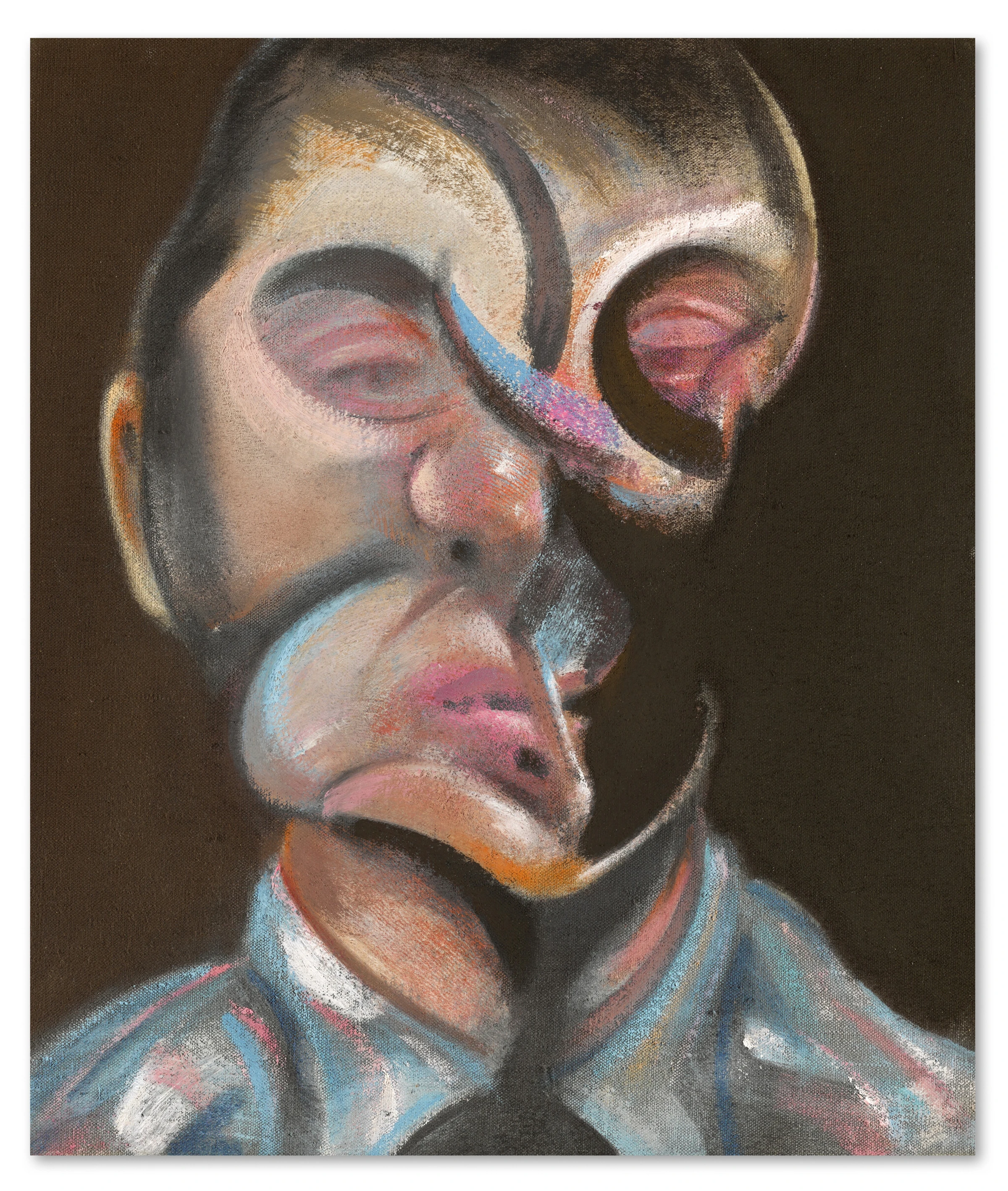

One headline lot, Francis Bacon’s 1972 Self-Portrait, reached about £16m, and Christie’s set a strong mark for Henry Moore’s King and Queen. Yet the stronger signal was not the top-price theater. It was the ability of less spectacular works by canonical names to clear at stable levels. That pattern suggests a buyer class prioritizing capital preservation, liquidity options, and downside control over short-cycle speculation.

The contrast with ultra-contemporary behavior is now hard to ignore. The post-pandemic burst in very young names was built on compressed timelines, thin historical pricing data, and a risk appetite often amplified by adjacent digital-asset exuberance. As that environment cooled, demand rotated toward twentieth-century artists with longer valuation histories, stronger institutional anchoring, and more predictable lender acceptance. In practical terms, that means Picasso, Bacon, Moore, and peers are increasingly handled as financial infrastructure inside private-wealth portfolios.

This is where auction data links directly to credit markets. Specialist and private-bank lending against art has expanded as collectors avoid taxable sales while unlocking liquidity. In that framework, a blue-chip painting is not only an object of cultural prestige, it is a balance-sheet instrument that can support borrowing capacity. Reports from market finance tracking, including the Deloitte Art & Finance research program, continue to show growth in art-secured lending channels even when transaction volumes soften.

Estate planning dynamics reinforce the same direction. As significant collections move through intergenerational transfer, heirs and advisors are reassessing holding structures, tax timing, and sale sequencing. That typically benefits works with deep institutional literature, transparent provenance, and broad global demand. Auction houses are adapting accordingly, placing greater emphasis on quality-vetted consignments, guarantee architecture, and lower-volatility lot mixes for marquee sessions.

For the trade, this is an important strategic shift. If buyers treat top-tier works as collateral-grade assets, then catalogue quality, condition documentation, and legal clarity become even more central to performance. Marketing language alone will not bridge weak provenance or technical doubt. At the same time, this environment can narrow oxygen for emergent artists unless galleries and institutions deliberately sustain risk-taking outside auction circuits.

The March signal from London is therefore double-edged. Confidence has returned at the top, but confidence is being allocated differently than during speculative peaks. The market is rewarding reliability, not hype. For collectors, the playbook is becoming less about chasing velocity and more about underwriting resilience. For artists and institutions, the open question is whether that capital discipline ultimately stabilizes the ecosystem or concentrates value even more tightly around already established names.

One practical implication is that advisory work has to become more forensic. A client buying into this market should ask not only whether a lot is good, but why this lot is surfacing now, who is underwriting downside, and what the probable exit routes look like in two to five years. Those questions used to be private-equity language imported into art. They are now standard market hygiene. If spring momentum continues into New York and Hong Kong with similar lot quality, the 2026 narrative will be clear: the high end is alive, but it is being priced by risk professionals as much as by taste-makers.