London’s March Sales Show the Ultra-Blue-Chip Market Holding Firm Despite Geopolitical Shock

Major evening auctions in London delivered strong totals and high sell-through, suggesting that demand for proven twentieth-century names remains resilient even as macro and geopolitical volatility intensifies.

London’s latest modern and contemporary evening sales produced a result the market had not fully priced in: confidence at the top end held, and in some cases strengthened, even as geopolitical risk escalated across multiple regions. Strong totals at Sotheby’s and Christie’s do not prove a broad market recovery, but they do clarify where conviction currently sits, blue-chip works with deep art-historical legitimacy, institutional familiarity, and collateral value in private banking ecosystems.

The headline numbers mattered less than the composition of demand. High sell-through rates were supported by guarantees and active lot management, but bidding energy was still visible on material that collectors and advisers classify as durable cultural capital. That includes established twentieth-century names where scholarship, museum visibility, and long-term resale pathways are already mature. In other words, this was not momentum driven by novelty, it was allocation behavior under uncertainty.

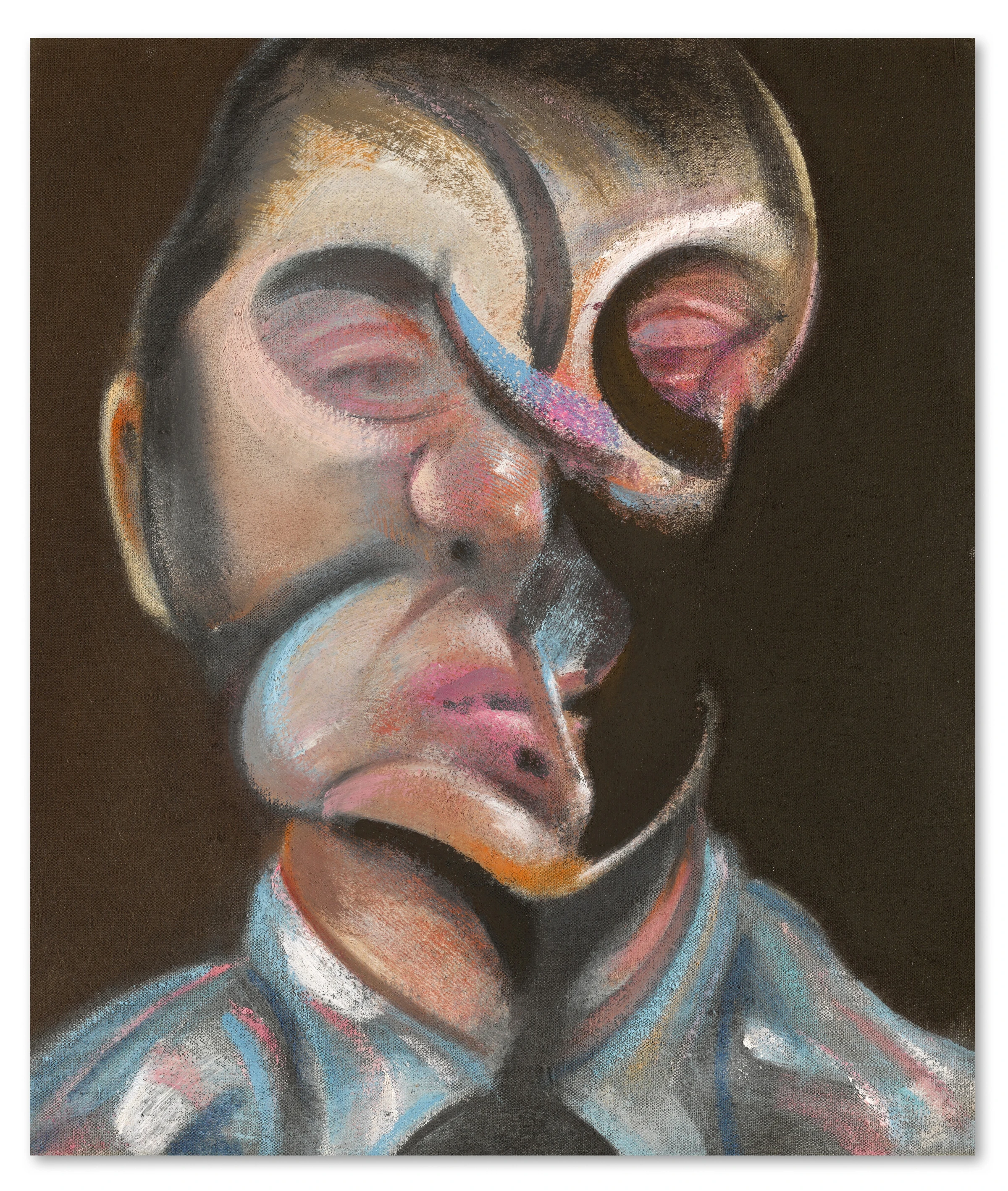

The Francis Bacon self-portrait that led discussion at Sotheby’s is a useful case study. Its pricing reflected more than object-level quality. It reflected confidence in category, in provenance architecture, and in the ability of canonical postwar artists to function as stores of value for globally mobile capital. Similar dynamics were visible across other marquee lots where bidding stayed disciplined but committed, indicating that top buyers are selective, not absent.

At Christie’s, the pattern echoed: serious money for established names, thinner enthusiasm for speculative edges. This bifurcation has been developing for several seasons, but London’s March performance made it explicit. The market is not treating all contemporary production equally, it is separating historically anchored assets from short-cycle narratives that rose rapidly in the post-pandemic surge and corrected just as quickly.

For advisers and family offices, this environment rewards sober portfolio thinking over trend chasing. Works that can be defended through scholarship, exhibition history, and cross-generational demand now look structurally stronger than works priced mostly on heat. That does not mean experimentation disappears. It means risk budgets are being reallocated, with primary and ultra-contemporary exposure handled more cautiously while blue-chip positions are reinforced.

The finance layer is critical here. Art-backed lending has become a larger part of how high-net-worth collectors manage liquidity, and lenders prefer assets with clearer valuation confidence. Reports from major wealth and art-finance channels, including frameworks used by houses such as Sotheby’s Financial Services, reinforce how established works can operate inside broader credit strategies. That reality feeds back into auction demand, because collateral-friendly art draws deeper pools of bidders.

There is a cultural consequence to this market logic. When capital concentrates in already-canonical artists, institutions and galleries need to work harder to sustain pathways for younger or less market-proven voices. Otherwise, public programming and market pricing diverge too sharply, with museums carrying experimentation while auctions consolidate around historic safety. That split is not fatal, but it can distort how value is interpreted across the sector.

London’s March auctions therefore should be read as a stress test result, not a victory lap. The test suggests the upper tier can still clear at meaningful levels when inventory quality is high and risk is well structured. It does not suggest the entire market is healthy, nor that demand has normalized across categories. For now, the center of gravity remains clear: quality, provenance, and institutional legibility are commanding the premium.

As spring sales continue, the key question is whether this pattern remains concentrated in exceptional lots or broadens into mid-tier segments. If it stays concentrated, the sector will continue operating in a two-speed regime, robust at the top, cautious below. If it broadens, confidence may be rebuilding more widely. London gave the first signal. New York and Hong Kong cycles will determine whether it becomes trend.